With new rates, NSSF will be swimming in money

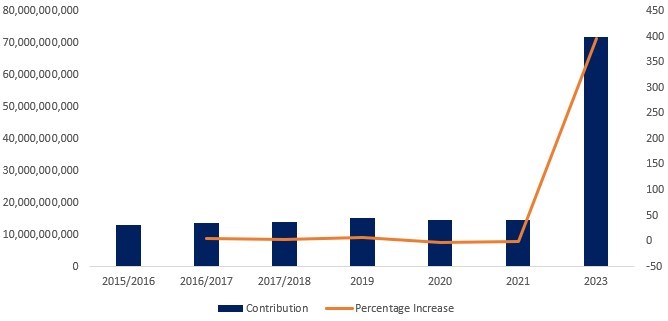

The calculation is based on an average of the graduated annual increase in contributions following the clearance of the legal hurdles that had prevented the implementation of the NSSF Act 2013.

The National Social Security’s purse will increase five-fold when the new enhanced contributions start this month.

The State-owned pension scheme could see its annual member contributions increase to approximately KSh71.93 billion annually, marking a 397% per cent increase from the KSh14.47 billion collected in the last reported year.

The calculation is based on an average of the graduated annual increase in contributions following the clearance of the legal hurdles that had prevented the implementation of the NSSF Act 2013.

Deductions will be calculated based on salary bands, with the initial starting with the lowest at KSh720 for those earning KSh6,000 to KSh1,800 for those earning KSh15,000 and KSh2,160 for those earning KSh30,000 and above.

The average contribution as calculated by the Moolah team will be KSh1,110 for each of the 2.7 million members and their employers.

NSSF is bound to have their own projections of the enhanced collections but the upshot of the new rates is that the institution will have much more money at its disposal than it had before.

The move to increase the rates has mostly been driven by complaints about the low payout for retirees, with President William Ruto putting the matter top of his agenda after he took power in late 2022.

“There is no retired Kenyan today who is living on their NSSF retirement benefits. The meagre current contribution of KShs.200 a month adds up to KShs.72,000 over 30 years. There is no rate of return on earth that can grow this into an adequate pension,” President Ruto told Parliament in an address in September 2022.

The World Bank has also supported the move, saying in a Kenya Economic Update that enhanced social protection will have a meaningful role in the country’s inclusive growth if, among other policy changes, the NSSF Act is amended to allow for higher contributions to the scheme by workers.

However, the World Bank said it wants to see these contributions protected through stricter regulations covering NSSF’s administrative costs and the facilitation of better returns on pension savings.

As the contributions increase exponentially, the big question becomes whether NSSF has the capacity to manage the funds and assure workers of a payout when retirement comes.

In the 1990s and early 2000s, the Fund was broke and struggled to pay pensioners money they had saved over decades.

Reports by the Auditor-General have revealed a number of shortcomings like when financial statements reflect several balances that are not adequately supported with appropriate records and information, as well as operational inefficiencies.

For instance, the latest Auditor-General report revealed that NSSF managers concealed investment revenue amounting to KShs.16.6 million from corporate bonds of a company listed on the Nairobi Securities Exchange (NSE). The amount was not entered in the Fund’s cashbook.

The audit report further flagged irregularities with the Fund’s bank overdraft which showed an overdrawn cashbook balance amounting to KShs.206.9 million, although this was not updated in the cashbook nor balanced against other entries.

The Fund has also been accused of accumulating expenses that exceed its total assets. The NSSF Act 2013 caps NSSF to accumulating expenses not exceeding 1.5 percent of its total assets.

Investments

Analysts say, for NSSF to better serve the interests of all stakeholders, there need to be proactive measures around increasing efficiency and cutting down on unnecessary expenditure, and it should invest the savings in high yielding investments in order to motivate employees in formal and informal sectors to save for their retirement.

The audit report states that in the financial year 2020/2021, the Fund’s investment income increased by 240.7 percent to KSh32.7 billion, translating to a Return on Investments of 11.9 percent. This was a significant increase from the previous year, when the Return on Investments was 4 percent.

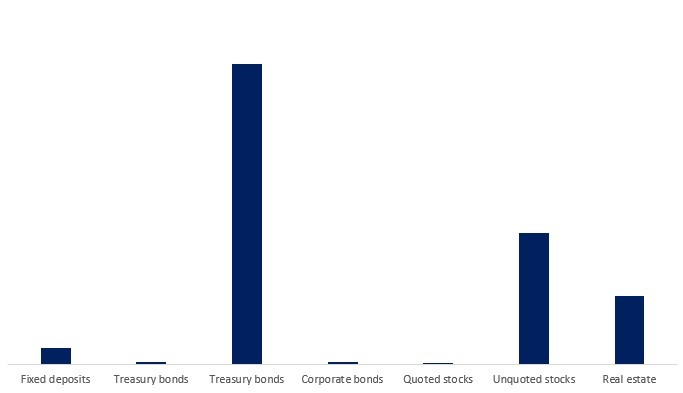

NSSF invests its funds in various financial instruments such as fixed deposits, Treasury Bills and Bonds, Corporate Bonds, Stocks, and Real Estate. In the year ended June 2021, the Fund collected a total of KShs.14.47 billion from its 2.7 million members and the net income earned from the Fund’s investments amounted to KShs.32.7 billion which is higher than the net income earned in the previous year.

Source: NSSF 2021 Annual Report and audited financial statements

However, in 2022, NSSF, more than doubled its holding in government securities in five years, and this signaled a leaning towards higher guaranteed returns in a market where listed equities have been generating lower returns and increased volatility.

Industry data showed that NSSF had grown its stake in Treasury bonds and bills to KSh170.9 billion last year from KSh83.2 billion in 2017. Government debt instruments have cash return ranging from 7.4 percent to 15 percent depending on the duration.

The Fund has been steadily increasing its stake in various blue chip companies listed at the NSE, eyeing its stable fundamentals and regular dividend payments that complement investment income from government securities.

NSSF is the biggest local institutional investor in the stock market, holding significant stakes in multiple firms directly and through its appointed fund managers.

The new contributions will greatly increase the amount of money that NSSF collects from its members. NSSF also wants to tap into President Ruto’s proposed incentive to give informal contributors up to KShs.3,000, a year if they save at least KShs.500 a month. The management also says if the Fund is able to sign up at least two million of the over 15 million informal sector workers, NSSF can get more money and grow its investment on NSE from the current KShs.65 billion to KShs.180 billion.

The government is also banking on the build-up NSSF collections to help finance some of its projects like the affordable housing agenda.

President Ruto has also indicated the government’s intention to reduce foreign borrowing and to depend more on local sources, such as NSSF.

“Part of the reason why we have borrowed heavily from others is because we have not been prudent in saving for our own country. We have to be prudent about saving. It is Biblical to save,” he said.